Introduction

A common thinking error from student years and early career often persists unnoticed for many years. Income is not understood as capital, but as monthly spending capacity. This error is convenient, socially accepted, and highly damaging to wealth.

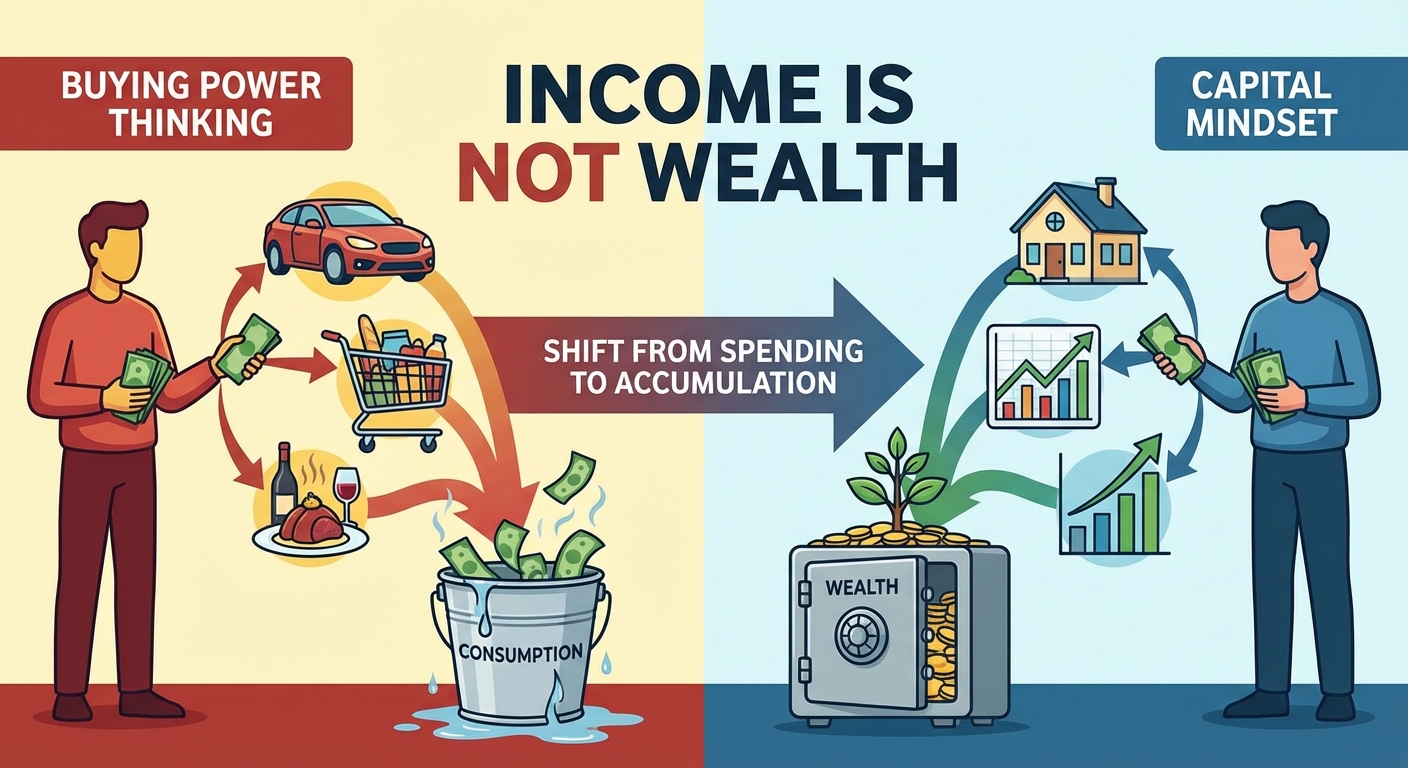

The thinking error: Income as exploitable buying power

Those who think about income primarily through affordable monthly payments are not optimizing for wealth. They are optimizing for consumption.

The pattern is simple:

- Fixed costs are subtracted.

- The remaining amount is mentally marked as freely available.

- This amount is committed through subscriptions, installment purchases, and loans.

- Salary increases do not increase capital, but monthly obligations.

This creates the illusion of progress. In reality, future income is simply being advanced and locked up.

Why this thinking systematically prevents wealth

This model makes someone an ideal consumer, but a poor wealth builder. It maximizes lifestyle, not freedom.

Wealth does not mean being able to afford things.

Wealth means owning assets that work for you.

Those who understand this evaluate status symbols differently. An expensive car often signals high fixed costs, not high assets. Even very high incomes do not protect against poverty if they are exclusively translated into consumption.

The perspective shift: Money is capital

The decisive step is to view income not as spending capacity, but as potential capital.

The question is not:

What can I afford monthly?

Instead:

How much of my income can I permanently turn into capital?

This perspective shift changes every financial decision. Consumption suddenly competes not with leisure time, but with returns.

Why future thinking was right, but wrongly applied

The original idea of viewing money through its future value was not wrong. It was just applied to consumption instead of capital.

A comparison makes this clear:

- 100 euros consumed monthly are simply spent after seven years.

- 100 euros invested monthly grow significantly through returns and compound interest.

The difference arises not through frugality, but through structure. Capital works. Consumption disappears.

Capital growth also changes emotions

Contrary to widespread assumption, consumption does not make you happier long-term than wealth building. On the contrary.

Capital building creates:

- a feeling of progress

- control over the future

- joy in exponential growth

Even market phases with price declines lose their terror when time is the most important ally. Falling prices become favorable entry points, not threats.

Wealth building is not sacrifice, it is a leveraged game

The real appeal arises when you start modeling the effects.

How high are future distributions?

What freedom arises in addition to pension?

What options open up as a result?

Capital thinking shifts focus from short-term consumption to long-term design.

Conclusion

Those who think of income as buying power remain dependent on income.

Those who think of income as capital build independence.

The difference lies not in earnings, but in the mental model.